Should I Pay Off My Mortgage Early?

If you want to make someone either really happy or really mad, tell them

a) pineapple belongs on pizza

b) you paid off your 3% mortgage early.

ARE YOU OUT OF YOUR MIND!!!!???

Pineapple-on-pizza debates aside, the question of paying off your mortgage early is uniquely polarizing right now as U.S. homeowners are sitting on an unusually broad range of interest rates.

Blanket arguments often fall on deaf ears as 6%'ers argue with 3%’ers who argue with 18%’ers who paid off their $64,000 homes back in 1997.

Additionally, whereas Americans as a whole love our debt and keep racking up more of it, a small remnant maintains their mission of living debt free - mortgage included (I should probably name drop Dave Ramsey here to help with SEO traffic), and no amount of persuasive math is going to stand in their way of screaming I’M DEBT FREE!!!!

So, what about mortgages?

Should you pay your mortgage off early, or should you pay the monthly minimum for 30 years and invest the difference?

It depends on whether you prioritize “math and money” or “peace of mind.”

I posed this mortgage question on Facebook and received this reply,

“Yes! Pay it off as quickly as you can. It is a wonderful feeling.”

Sounds like a “peace of mind” person to me.

Another person on Instagram commented,

“Not if it’s under 3%.”

Sounds like a “math and money” person to me.

I love a healthy debate.

Let’s talk about it and see if we can’t find some common ground around our desires for risk mitigation, peace of mind, and making wise financial decisions.

Three primary money and math considerations:

Mortgage interest rate

Mortgage term

Investment return rate

Why do these matter?

Many homeowners will pay MORE in interest than they pay on principal.

This is fairly simply math, and I break it it down to show the cost of interest at varying rates in a spreadsheet here.

A 30-year $500,000 mortgage at 6% interest will

include $579,190.95 in total interest paid.

Loan amortization schedules.

Most mortgage interest is paid during the first half of the mortgage term, so paying extra money toward your mortgage principal each month greatly reduces the amount of interest paid over the life of the loan AND how many years you’ll need to make a monthly payment.

Paying an extra $400/mo on a 6%, 30 year, $500,000 mortgage will pay it off 7 years and 9 months earlier and save $172,466 in interest.

Contrast those graphs with one of a 15 year mortgage which requires a higher monthly payment, allowing more of the payment to be allocated toward rapid "principal reduction” instead of interest.

There can be big savings in paying off a loan faster.

Instead of paying $579,190.95 in interest over 30 years, a homeowner only pays $259,471.15 over 15 years.

Investment interest rates require TIME to effectively compound.

A mortgage starts with a large balance and gets smaller, which is why it makes sense that there is more interest PAID during the first half of the term.

Inversely, investment account balances start small and increase over time, so the latter half of the term EARNS greater returns than the first.

(You can learn more about that in an article I wrote about how to become a millionaire.)

This is why the investment return rate must be considerably higher than the mortgage interest rate - because interest is SAVED when a mortgage is paid off early, but interest is EARNED when investment returns have time to compound.

Three Primary “Peace of Mind” considerations:

Moral values.

Many people are generally debt averse and feel more at peace knowing their home (or car or…anything) is paid off. For some, this includes a moral component of seeking to apply biblical passages about how “borrowers are slaves to the lender.”Risk mitigation.

Even with low interest rates, there is risk to consider when taking out a loan. A bank is no more forgiving of missed payments on a 2% interest rate than an 8% interest rate.Guaranteed returns.

A person who pays off their mortgage early can run the exact numbers to know how much money they are saving by paying it off early. No guesswork required.

Why would you NOT pay off your mortgage early?

The main reason is some version “I want to use that money for something else,” even if that something else is just keeping food on the table.

For the sake of this article, let’s assume the choice is intentional and the homeowner COULD pay extra if they wanted to.

Rather than applying an extra payment toward their mortgage each month, some homeowners prefer to invest that money and increase their “liquid” (accessible cash) savings.

You desire liquidity instead of home equity.

That’s a nerdy way of saying you prefer to have $100,000 cash in the bank instead of owing $100,000 less on your home.

If unexpected emergency bills arise, there is an advantage to having money available in the bank to withdraw instead of having it all tied up in your home’s equity.

(Yes, I know you can access your home’s equity through a HELOC or HELOAN, but that assumes you qualify in the moment of need and can afford to pay the interest).You (potentially) forfeit annual mortgage interest as a tax deductible expense.

Mortgage interest is tax deductible, so by paying off your mortgage early, you are foregoing that as a contributing factor if you hope to itemize your deductions each year (talk to your CPA about this one).

So, SHOULD you or SHOULDN’T you pay off your mortgage early?

You SHOULD, if and only if…

You have an established financial safety net. This amount varies from person to person, but the generally advised best practice is 3-6 months. For single-income families with children, I’d recommend you have at least 6 months of emergency reserves. For single people or families with multiple income earners, you might choose to only set aside the 3 months safety net.

You have paid off all other short-term (and likely variable or higher interest rate) debt. Credit cards and car loans are most common and should be paid off before any extra money is paid toward your home mortgage.

Your interest rate is 5% or higher. Mathematically, a 5% interest rate is the break even point between potential interest earned and mortgage interest saved, and assumes…

a) you will pay a 15% long term capital gains tax rate on the interest earned

and

b) you will earn an 8% annual return on investment. Note: Over the last 20 years, the average returns of the stock market S&P 500 is 10%. After accounting for taxes and a shortened amortization calendar, it will require about a 3% margin between your mortgage interest rate and your rate of return to come out ahead financially so that you earn more in interest than you save by making early payments.

BECAUSE OF TAXES OWED ON INVESTMENT INTEREST EARNED

AND

BECAUSE OF THE ABBREVIATED AMORTIZATION SCHEDULE CAUSED BY MAKING EXTRA PAYMENTS ON YOUR MORTGAGE,

IT’S NOT ENOUGH TO HAVE THE RATES MATCH.

These are the #1 mistake I see people make in their calculations. Taxes owed on interest earned and the implications of a shortened loan pay off period.

CASE STUDY

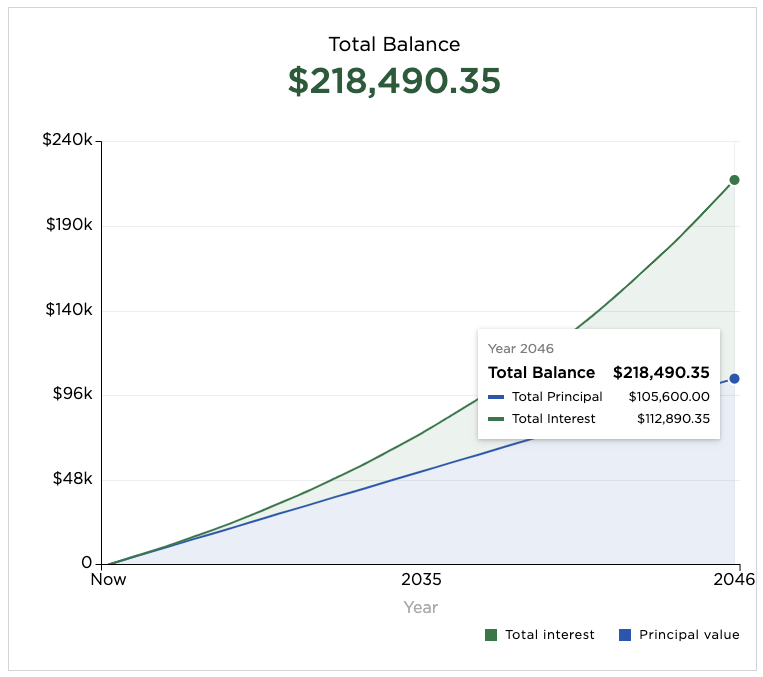

Let’s assume you have a $500,000 mortgage, a 30 year term, a 6% interest rate, and $400 a month in extra money to decide what to do with.

If you apply the $400/mo to your mortgage, you will save $131,473 in interest and pay off your mortgage in just 22 years, 3 months.

If you invested the money at an 8% return, you would earn $181,115.25 ($152,947 after taxes) in interest, PLUS have a $105,600 nest egg ($400/mo x 264 months) you could use to pay down the remaining mortgage principal if you wish - and leave you with $22,475 left over.

Which in 22 years will be enough to buy you probably one dozen eggs and a bottle of ketchup (I’m kidding…I hope).

For the money and math folks, once you factor in risk and inflation, $22,000 over 22 years isn’t that much. A win is a win, but barely.

If you value peace of mind, consider the peace of mind that comes with having a 6 months safety net PLUS $100,000+ in cash stashed away (so you COULD pay off your home if you wanted to) earning interest in a High Yield Savings account where the principal is protected, or in another investment account earning more than you’re paying in interest.

Seriously, I geeked out and made a super nerdy Google spreadsheet if you want to check it out.

It breaks down various interest rates, return on investment, and tax brackets.

If it’s too confusing (and it might be the case), feel free to email me and I’m happy to talk through your situation with you.

If you have a desire to buy or sell in the coming year, let’s chat.

Life has a way of keeping us all moving, and I’d love to be your real estate agent.

Contact me here to set up your free and confidential consultation.

Kevin